The private credit boom—now topping $2 trillion globally—has filled crucial gaps left by post-2008 bank regulations, offering flexible financing to mid-market companies at yields of 8-12%. Yet, as AI disruptions loom and redemptions rise, vulnerabilities like illiquidity and light oversight are surfacing.

Look at recent headlines: BlackRock limited 95% of a $1.2 billion withdrawal in its $26 billion HPS fund, Blackstone dealt with 7.9% outflows in its $82 billion vehicle (with executives ponying up $150 million personally), and Blue Owl suspended redemptions in a $1.6 billion tech-focused fund. These events underscore a need for reform.

Enter India's Non-Banking Financial Companies (NBFCs): a parallel non-bank lending sector that's grown resilient under the Reserve Bank of India's (RBI) rigorous framework. By borrowing from this "playbook," U.S. private credit could enhance stability, curb systemic risks, and protect investors without stifling innovation. Here's a deep dive into the risks, key players, and actionable lessons.

Understanding the Risks: Why Private Credit Needs a Stability Upgrade

Private credit thrives on direct loans to leveraged or underserved borrowers, bypassing banks' constraints like Dodd-Frank. Its strengths—speedy execution, tailored covenants, and higher returns—are offset by structural weaknesses. Illiquidity is inherent: Funds often impose gates or quarterly redemption limits (e.g., 5%), leading to "run-like" scenarios during stress. Regulation via the SEC focuses on adviser fiduciary duties, anti-fraud measures, and disclosures (e.g., Form PF for monitoring), but lacks prudential safeguards like capital buffers or leverage caps—opening doors to aggressive practices, such as covenant-lite loans (80-90% of deals) and payment-in-kind (PIK) structures (20-30% of portfolios), which can hide brewing defaults. The market's scale amplifies this: $2 trillion in AUM ($1.3 trillion U.S.), up from $500 billion in 2015, with $400 billion+ in dry powder driving competition and looser terms. Recoveries remain solid (65%+ for senior loans), but adjusted non-performing loans (NPLs) hit 3-5.8%, far above banks' 0.3-0.9% average (e.g., Bank of America at 0.3%). UBS projects up to 15% defaults in 2026 from AI and rate pressures.

India's NBFCs, managing ~$700 billion in assets with 15-20% annual growth, mirror this but under RBI's Scale-Based Regulation (SBR). They enforce 15% capital adequacy ratios (CRAR), 5-7x leverage limits, asset classification, and liquidity reserves—prioritizing risk mitigation over just fraud prevention. This has helped NBFCs weather crises like the 2018 IL&FS fallout, offering a blueprint for private credit to build resilience without the capitulation to complete banking style reforms which would take away the advantage of being a private credit fund in pricing and flexibility.

Key Players and Exposures: Pinpointing Vulnerabilities for Targeted Reforms

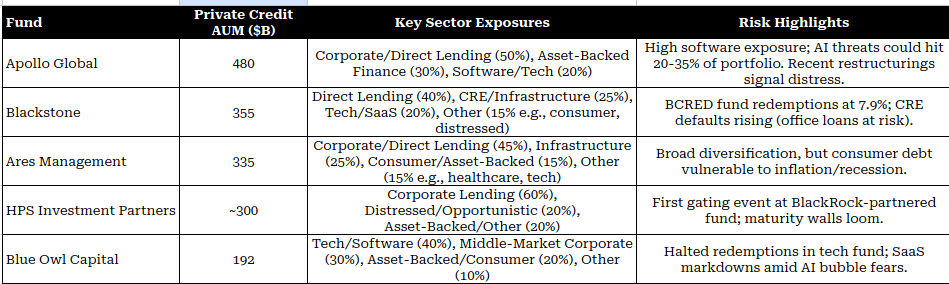

Dominant firms (as outlined in the image) control much of the market, with exposures skewed toward high-risk sectors. Market-wide, direct lending leads (~55%), followed by asset-backed finance (20-30%), infrastructure/real estate (15-25%), and distressed/opportunistic (10-15%). Tech/software (20-40%, often small-mid cap) is acutely at risk from AI, while CRE grapples with vacancies. Healthcare (93% lender interest) and business services (79%) offer buffers but face economic drags.

These breakdowns reveal hotspots:

a. Tech (20-40%) risks AI obsolescence (25-35% vulnerability per UBS) b. CRE (15-25%) faces $12.7 billion in 2026 maturities (up 73% YoY) c. asset-backed (20-30%) could falter on inflation. and d. Opportunistic structured loans to stressed companies are risky by definition

Funds with high private credit concentration (e.g., Blue Owl at 62%) are most exposed to a multitude of these risks.

Systemic Interconnections: Why NBFC-Style Oversight Could Prevent Spillovers

Private credit ties deeply with banks: $300 billion in U.S. bank lending (up 145% since 2020), plus $340 billion in commitments. Wells Fargo tops at $60 billion, but JPMorgan leads broader non-depository exposures ($47 billion to PE, including private credit), with Citi, Bank of America, Goldman, and internationals like Barclays/RBC sharing the load.

Second-order effects abound: Apollo defaults could trigger $2-3 billion losses for partners like Citi, rippling through $1.57 trillion in NDFI loans—even non-direct banks feel it via shared ecosystems. Retail access via BDCs/ETFs heightens volatility. RBI's NBFC rules curb such interconnections through exposure limits and systemic monitoring, a model the SEC or FSOC could emulate.

Actionable Measures: Adopting NBFC Principles for a Safer Private Credit Ecosystem

To evolve, private credit should integrate RBI-inspired elements:

1. Mandate Capital and Leverage Buffers: SEC/FSOC could require 15% CRAR and 5-7x leverage caps for advisers over $150 million AUM, ensuring funds withstand shocks. Contractually, investors could stipulate similar ratios in fund docs.

2. Enforce Provisioning and Asset Classification: Adopt RBI's tiered norms (e.g., 0.25-5% reserves based on risk), classifying loans by delinquency to flag issues early. Funds could embed quarterly provisioning in agreements, reducing "shadow defaults."

3. Boost Liquidity Management: Require 15-30% high-quality liquid assets, like NBFCs, to handle redemptions. Contracts might include mandatory buffers or stress-tested gates.

4. Cap Sector Exposures: Limit tech/CRE bets to 20-25% per fund, mirroring RBI's diversification push, to mitigate AI or vacancy risks.

5. Enhance Disclosures and Oversight: Expand Form PF to include interconnectedness reports, with RBI-style inspections for large players.

These steps—regulatory or contractual—could lower NPL gaps, contain spillovers, and sustain growth to $3-4 trillion by 2030.

By emulating NBFCs, private credit can mature into a more robust asset class, again, without sacrificing what makes private credit, private credit. This is not to say there is a necessity for regulatory oversight - institutions may just enable these guardrails internally. Thoughts?

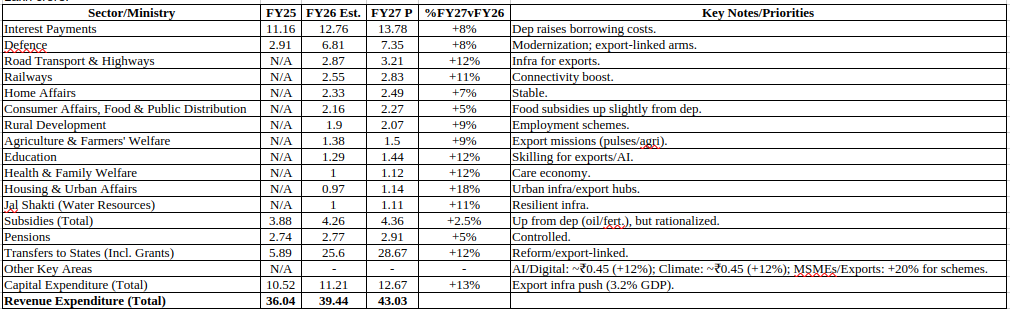

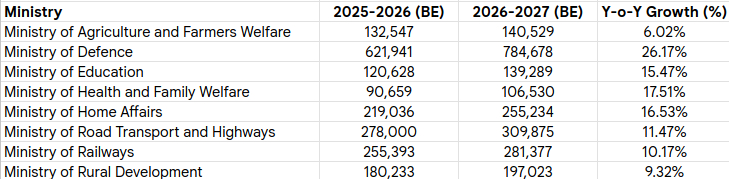

Final FY2026 Budget Summary

Final FY2026 Budget Summary